# Are Bitcoin ETF Managers Doing A Good Job (Part 1)?

Source: https://www.yieldcurve.pro/blog/btc-etf-tracking-error-001

Published: 2024-03-25

Tags: ARK, ARKB, BITB, BRRR, BTCO, BTCW, Beta, Bitcoin, Bitwise, Drawdown, ETFs, EZBC, FBTC, Fidelity, Franklin Templeton, GBTC, Grayscale, HODL, IBIT, Invesco, Tracking Error, Valkyrie, VanEck, WisdomTree, iShares

_Taking a look at how closely the new ETFs track Bitcoin_

# Are Bitcoin ETF Managers Doing A Good Job?

Early in our career, we were responsible for managing a variety of different

equity index funds. If you were doing your job correctly, investors in those

funds could expect to enjoy single digit tracking errors.

Tracking error is simply the annualized standard deviation of the difference in

daily returns between two different assets **1** and **2**:

$$TE = \sqrt{\frac{252}{N-1} \sum_{i=1}^{N} (R_{1,i} - R_{2,i})^2 }$$

Obviously, the smaller the tracking error the tighter asset 1 tracks

asset 2. A tracking error of zero implies perfect replication of returns.

Recently, a number of institutional asset managers have launched a set of

exchange-traded funds (ETFs) designed to track the Bitcoin crypto currency. It

is natural to wonder how those ETFs are tracking as a group. Moreover, we are

curious to know which of them does the best job.

# Grayscale Bitcoin Trust

One of these ETFs did not begin that way. More specifically, the Grayscale

Bitcoin Trust ETF was originally launched as a trust in 2013 and offered to

accredited investors only. In 2015, it became a publicly ***quoted***

instrument.

Grayscale first attempted to convert the trust to an ETF in 2017, a process that

concluded on January 10, 2024 with approval for GBTC as well as for the

following set of managers:

| Ticker | Manager | AUM ($M) | Fee (BPS) |

| :----- | :------ | ------ : | ------- : |

| GBTC | Grayscale | $23,372 | 150 |

| IBIT | iShares | $15,681 | 25 |

| FBTC | Fidelity | $8,891 | 25 |

| ARKB | ARK | $2,633 | 21 |

| BITB | Bitwise | $1,956 | 20 |

| HODL | VanEck | $514 | 20 |

| BRRR | Valkyrie | $423 | 25 |

| BTCO | Invesco | $328 | 25 |

| EZBC | Franklin Templeton | $236 | 19 |

| BTCW | WisdomTree | $74 | 25 |

#### **Table 1**: Bitcoin ETFs, Managers, AUM, and Fee

GBTC has the distinction of being the oldest, largest, and most expensive

Bitcoin index ETF. Since it has the longest history we will use it to compute

a longer, rolling history of tracking error. We will then look at some of the

other funds and their performance since inception.

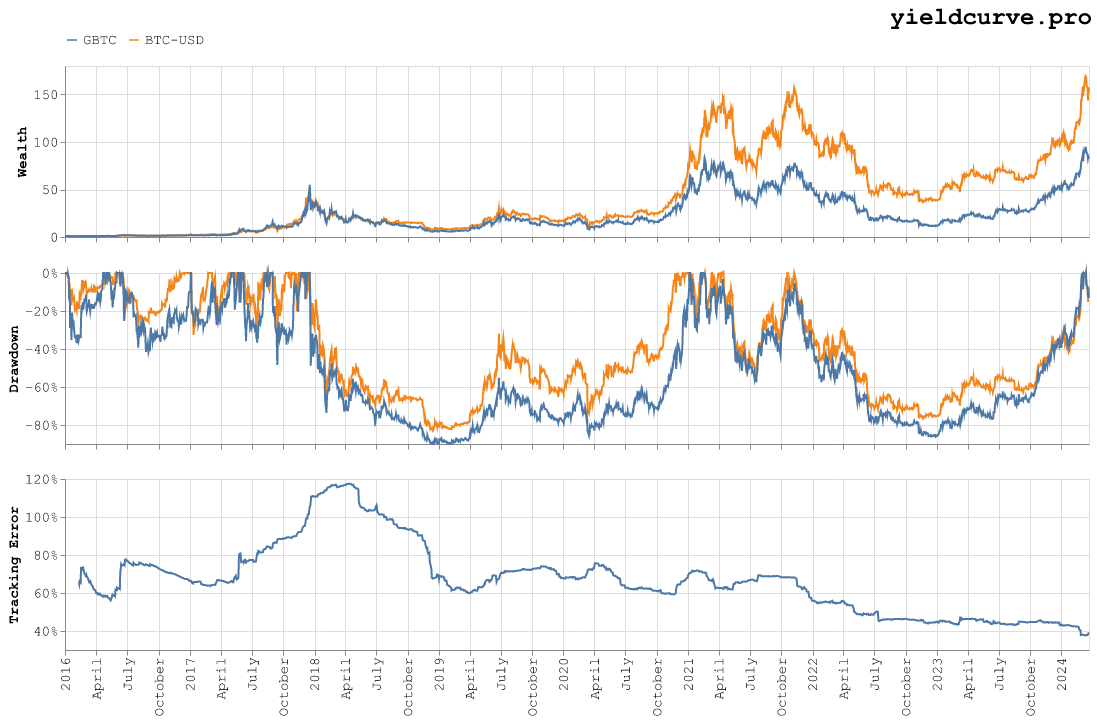

#### **Figure 1**: Wealth, Drawdown, and Relative Tracking Error (BTC-USD and GBTC)

It is apparent from the equity curves that GBTC has dramatically underperformed

spot. Table 2 shows the average annualized returns for each.

| Symbol | Arithmetic | Geometric |

|:---------|-------------:|------------:|

| BTC-USD | 83.16% | 80.91% |

| GBTC | 88.93% | 67.81% |

#### **Table 2**: Average Annualized Returns (2016 to Present)

Interestingly, GBTC had higher/lower arithmetic/geometric returns,

respectively.

As shown in Table 3, GBTC had larger average and maximum drawdowns.

| Symbol | Average | Maximum |

|:---------|----------:|----------:|

| BTC-USD | 39.57% | 83.01% |

| GBTC | 50.69% | 89.91% |

#### **Table 3**: Drawdowns (2016 to Present)

Turning our attention to rolling annualized tracking error, we see it increase

from about 60% at inception to a maximum value of 117% in early 2018. While

not monotonic, tracking error continues to decrease settling at a terminal

value of about 39%. These values are summarized by Table 4.

| Symbol | Minimum | Average | Maximum | Terminal |

|:---------|----------:|----------:|----------:|-----------:|

| GBTC | 37.67% | 67.19% | 117.55% | 39.15% |

#### **Table 4**: Tracking Error (2016 to Present)

As a manager, it appears that Grayscale has improved over time with a

noticeable inception-to-present reduction in tracking error.

# Other Managers

In order to arrive at an apples-to-apples comparison we are going to compute

tracking error for GBTC and the new ETFs in the same fashion. We will assume

that GBTC launches on the same day and compute rolling annualized tracking

errors using a minimum of 30 days of data.

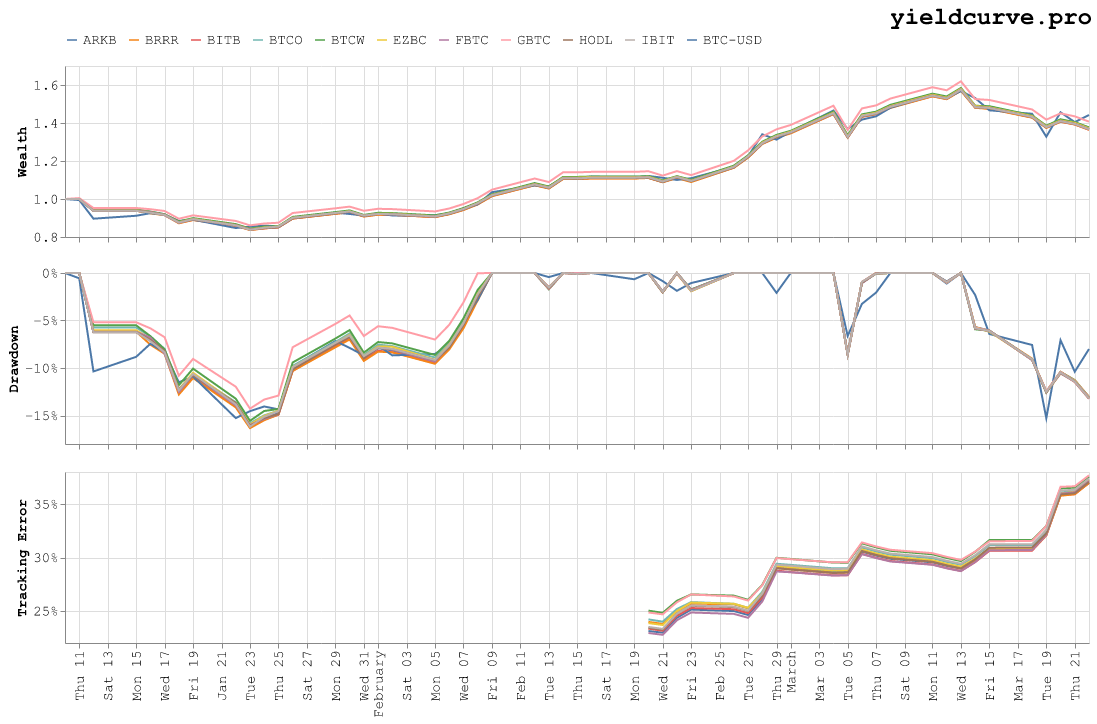

Figure 2 shows the Wealth, Drawdown, and Tracking Error charts for spot and

each ETF listed in Table 1.

#### **Figure 2**: Wealth, Drawdown, and Relative Tracking Error (BTC-USD and ETFs)

The equity curves for the ETFs seem to track each other fairly well. However,

the reader should notice that spot and GBTC are trading at a premium relative

to the other managers. Table 5 shows the average annualized returns since

launch.

| Symbol | Arithmetic | Geometric |

|:---------|-------------:|------------:|

| BTC-USD | 192.85% | 469.82% |

| ARKB | 164.46% | 344.73% |

| BITB | 162.78% | 337.73% |

| BRRR | 163.30% | 338.96% |

| BTCO | 166.51% | 354.60% |

| BTCW | 167.21% | 357.37% |

| EZBC | 165.56% | 349.71% |

| FBTC | 164.15% | 343.14% |

| GBTC | 177.24% | 407.19% |

| HODL | 164.19% | 342.95% |

| IBIT | 164.05% | 342.51% |

#### **Table 5**: Average Annualized Returns (January 10, 2024 to Present)

The difference between arithmetic and geometric is so pronounced it makes us

wonder if there is any point in reporting the latter.

Table 6 reports drawdowns for each asset.

| Symbol | Average | Maximum |

|:---------|----------:|----------:|

| BTC-USD | 5.03% | 15.28% |

| ARKB | 5.10% | 16.12% |

| BITB | 5.15% | 16.25% |

| BRRR | 5.18% | 16.33% |

| BTCO | 4.95% | 15.82% |

| BTCW | 4.86% | 15.56% |

| EZBC | 5.03% | 15.93% |

| FBTC | 5.09% | 16.00% |

| GBTC | 4.36% | 14.28% |

| HODL | 5.09% | 16.08% |

| IBIT | 5.06% | 16.18% |

#### **Table 6**: Drawdowns (January 10, 2024 to Present)

Spot and GBTC display the best drawdown characteristics.

Tracking errors (since inception) are shown in Table 7.

| Symbol | Minimum | Average | Maximum | Terminal |

|:---------|----------:|----------:|----------:|-----------:|

| ARKB | 22.97% | 29.05% | 36.98% | 36.98% |

| BITB | 23.14% | 28.97% | 36.98% | 36.98% |

| BRRR | 23.79% | 29.24% | 36.97% | 36.97% |

| BTCO | 24.00% | 29.53% | 37.28% | 37.28% |

| BTCW | 24.82% | 30.05% | 37.56% | 37.56% |

| EZBC | 23.69% | 29.35% | 37.24% | 37.24% |

| FBTC | 22.77% | 28.87% | 37.16% | 37.16% |

| GBTC | 24.68% | 30.06% | 37.69% | 37.69% |

| HODL | 23.26% | 29.18% | 37.07% | 37.07% |

| IBIT | 23.32% | 29.46% | 37.38% | 37.38% |

#### **Table 7**: Tracking Error (January 10, 2024 to Present)

Fidelity (FBTC) has the lowest average while Valkyrie (BRRR) has the lowest

terminal tracking error, respectively. It is intereseting to observe that,

since inception, tracking errors have increased steadily this year. Volatility

has been steadily ramping up so, as we will see, this is not too surprising.

# Discussion

We set out to try and assess if Bitcoin ETF managers are doing a good job.

Additionally, we were hoping to measure which of them was doing the best job.

Our measuring stick for determining this was tracking error. Visual inspection

of the equity, drawdown, and tracking error curves suggest our attempt to

measure manager efficiency has some problems:

- First, ETFs trade weekdays over a limited set of hours. As we all know Bitcoin

spot trades 24/7.

- Next, ETFs charge a management fee. We have listed these in Table 1 but have

made no attempt to adjust our calculations based on them.

- Last, unlike other traditional finance index products, managers in the crypto

space cannot rely on a market-on-close (MOC) auction to lock in consistent end

of day pricing. While it might make sense for them to transact at the

traditional TradFi MOC (to correspond with the ETF MOC) we have no intimate

knowledge of how or when these managers actually trade.

As far as we can tell the first two issues should not have material impact on

the tracking errors we see, simply based on their large magnitude. The last

one could make a significant difference, however.

Each manager tracking error is more-or-less the same magnitude. Because our

model is likely very imprecise we can't really say which is **best** or

**worst**. Instead, can we say they are all doing a **bad** job?

Since we are already conducting a noisy experiment there is nothing to stop us

from further muddying the analysis with some hand-wavy math. Let's start by

expressing tracking error using volatilities and correlation as follows:

$$TE^2 = \sigma_1^2 + \sigma_2^2 - 2 \sigma_1 \sigma_2 \rho$$

Let us say that:

$$\sigma_1 \approx \sigma_2 \approx \sigma$$

which, at least for an index product, isn't a horrible assumption. Actually,

it's a bit of stretch but here go. This simplifies tracking error a bit:

$$TE^2 = 2 \sigma^2 \left(1 - \rho\right)$$

Now, we want to compare tracking error for Bitcoin to an asset class we know

more about like equities. We can construct the following ratio:

$$\frac{TE_{BTC}}{TE_{SPY}} =

\frac{\sigma_{BTC} \sqrt{\left(1 - \rho_{BTC}\right)}}

{\sigma_{SPY} \sqrt{\left(1 - \rho_{SPY}\right)}}$$

This next assumption is likely a bad one but we won't let that stop us. We are

going to give our ETF managers the benefit of the doubt and say that the

different levels of tracking error are not due to differences in skill

relative to their equity manager brethren. This says that a given Bitcoin and

SPY ETF should have similar correlation with its index leading to:

$$TE_{BTC} \approx \frac{\sigma_{BTC}}{\sigma_{SPY}} TE_{SPY}$$

To a **very** rough approximation, an equally skilled Bitcoin index manager

should have a tracking error that is multiple of the equity counterpart where

the multiple is the ratio of their respective index volatilites.

At least this year, the ratio of volatilities has been approximately 5.6 so:

$$TE_{BTC} \approx 5.6 \times TE_{SPY}$$

As we said earlier, a skilled equity index fund manager can be expected to run

at a tracking error measured in the single digit basis point range. Even if we

increase the multiple in the above equation by an order of magnitude we will

not get anywhere near the values shown Table 7.

This most likely means one of two things:

- the Bitcoin ETF managers in Table 1 are God awful

- this hastily written analysis is total garbage

If it is the latter and/or you find some glaringly obvious mistakes in this

post, kindly shoot us a note. Moreover, anyone with intimate knowledge of how

these ETFs are managed please educate us. As we said, we know how it works on

the equity side but Bitcoin...not so much.

We have a

Feedback

page so please reach out.

Best -- YCP