# Examining Yield Curve Similarity (Part 1)

Source: https://www.yieldcurve.pro/blog/examining-yield-curve-similarity-part-1

Published: 2023-09-05

Tags: Distance Metrics, Interest Rate environments, Manhattan Distance, Yield Curve

_How to discover similar interest rate environments?_

# Examining Yield Curve Similarity (Part 1)

### Where Do We Sit Today?

The level of and change in the Yield Curve affects the economy

and return streams across the different asset classes. It's

a reasonable thing to wonder if historical data can be used to

decipher what will transpire in the future.

In order to conduct a study of that sort it would be helpful to

have a metric that says "these past environments are similar to

today's". When we speak of yield curves we typically think of

where it sits in yield space as well as it's shape.

So where does today's yield curve sit and what shape does it

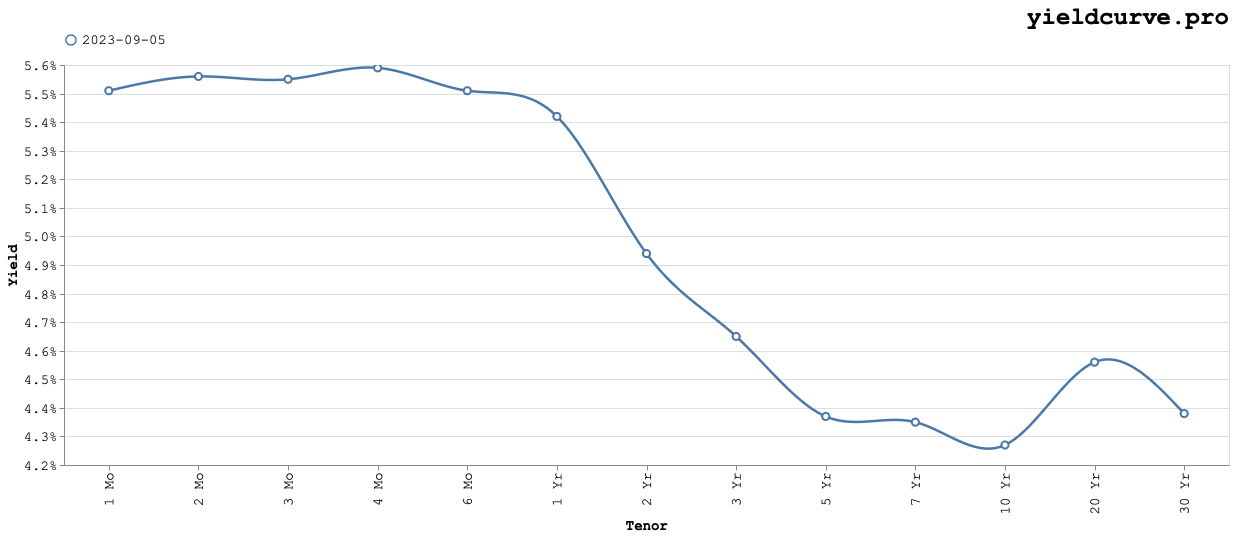

have. The following chart shows the yield curve as of

September 5th 2023.

The average yield sits somewhere just below 5% and the shape is

"inverted". From the 4-month to the 10-year tenor, rates decrease

monotonically with an odd local maxima (hump) at the 20-year point.

While the level, historically speaking, isn't that unusual the

shape is.

The average yield sits somewhere just below 5% and the shape is

"inverted". From the 4-month to the 10-year tenor, rates decrease

monotonically with an odd local maxima (hump) at the 20-year point.

While the level, historically speaking, isn't that unusual the

shape is.

### Metrics

One way to define similarity is to use a distance metric. One

could use a function of correlation

$$d(\rho) = \sqrt{2(1 - \rho)}$$

A naive approach, and the one we'll adopt, is to use the mean average

deviation (or normalized

Manhattan Distance)

between yield curves at two distinct dates

$$ d(\tau, t) = \frac{1}{N}\sum\_{i=1}^{N}|y_{i}(\tau) - y_{i}(t)|$$

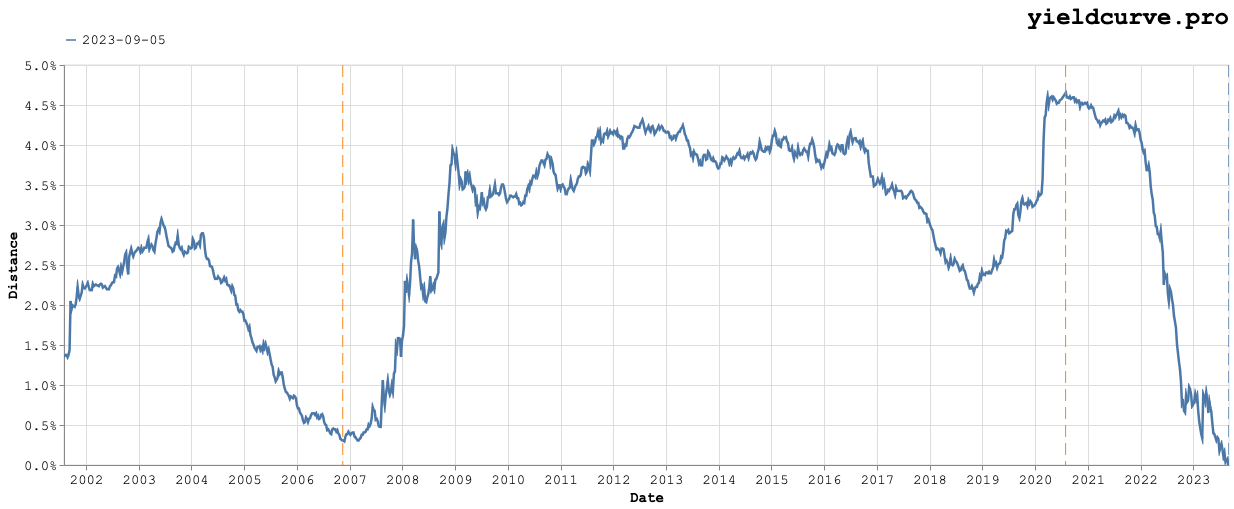

Notice that this distance is expressed in units of yield. Holding one

date fixed (at say, September 5 2023) and letting the other range over

all available data results in the following chart.

Obviously, the distance between the fixed yield curve and itself will

be zero. So, if we want to identify meaningfully similar yield curves

(i.e., smaller distances) at different points in time we need to begin

looking a certain number of days away from the fixed date. In this

case, we've arbitrarily chosen two quarters on either side. The vertical

dashed line in blue denotes the fixed date and the two orange lines

denote the dates with minimum and maximum distance.

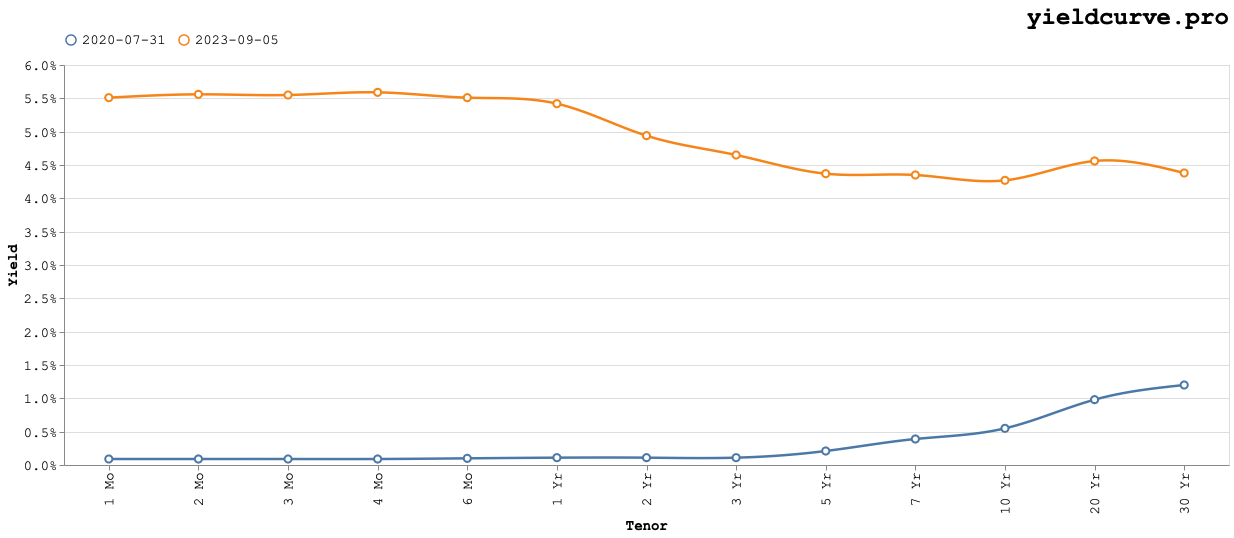

The maximum distance occurs on July 31, 2020 with the corresponding yield

curves shown in the following chart.

Obviously, the distance between the fixed yield curve and itself will

be zero. So, if we want to identify meaningfully similar yield curves

(i.e., smaller distances) at different points in time we need to begin

looking a certain number of days away from the fixed date. In this

case, we've arbitrarily chosen two quarters on either side. The vertical

dashed line in blue denotes the fixed date and the two orange lines

denote the dates with minimum and maximum distance.

The maximum distance occurs on July 31, 2020 with the corresponding yield

curves shown in the following chart.

These curves are on opposite sides of the yield space (level) and have

different shapes (slopes) as the older curve is upward sloping. In

this instance it seems our chosen distance metric works.

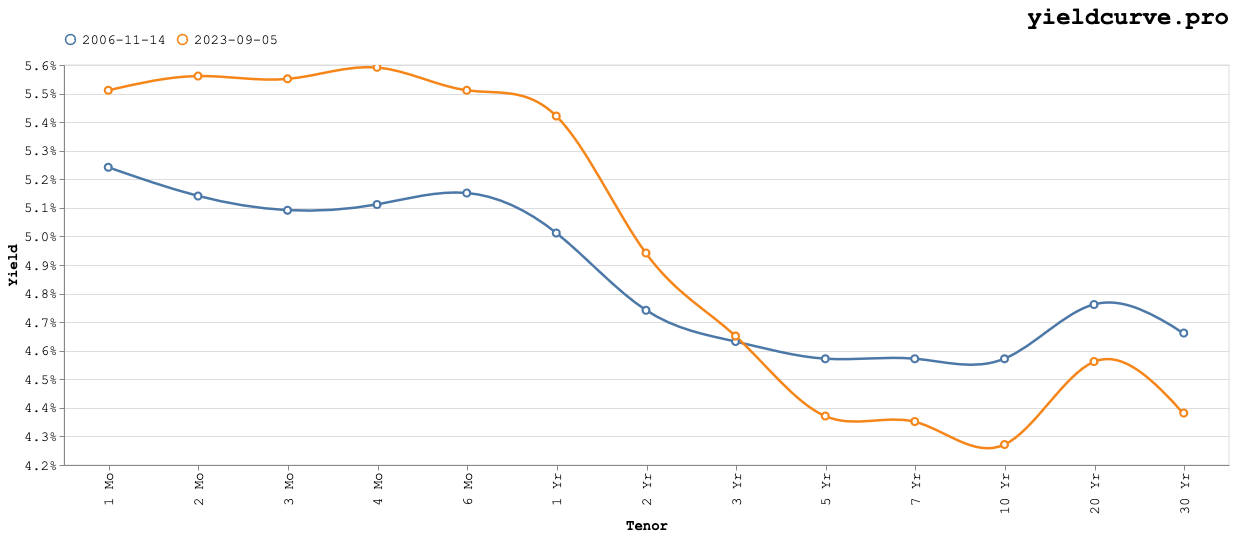

The minimum distance occurs on November 14, 2006 with the corresponding yield

curves shown in the following chart.

These curves are on opposite sides of the yield space (level) and have

different shapes (slopes) as the older curve is upward sloping. In

this instance it seems our chosen distance metric works.

The minimum distance occurs on November 14, 2006 with the corresponding yield

curves shown in the following chart.

Again, the distance metric appears to work as intended. Both curves are

centered around the same approximate level of 4.8%. Also, both curves

are inverted with similar slopes.

Again, the distance metric appears to work as intended. Both curves are

centered around the same approximate level of 4.8%. Also, both curves

are inverted with similar slopes.

### Conclusions

What conclusions can we draw from this? Do the curves with minimum

distance identify similar interest rate environments?

Unfortunately, similar level and slope are not enough. We have completely

ignored path dependency. Namely, what trajectory did each curve travel

to arrive at those configurations? And how would we go about measuring

those? Perhaps we can use the notion of

Bull, Bear, Flatteners, Steepeners?

We will leave that for a subsequenbt blog post.