# Treasury Auction Liquidity

Source: https://www.yieldcurve.pro/blog/treasury-auction-liquidity-001

Published: 2024-01-09

Tags: Auction, Bid to Coverage Ratio, Bills, Bonds, Cash Management Bills (CMB), Floating Rate Notes (FRN), Notes, Treasury Inflation Protected Securities (TIPS), US Treasury

_Monitoring US Treasury Auctions and Issuance to Estimate Security Liquidity_

# Monitoring US Treasury Auctions and Issuance to Estimate Security Liquidity

Figure 1 shows the first post of an excellent Twitter

thread

by

James Lavish.

#### **Figure 1**: "Time for a Treasury Thread."

#### **Figure 1**: "Time for a Treasury Thread."

In that thread James provides a primer on the mechanics of US Treasury (UST)

auctions. He begins by giving a refresher on some basic lexicon. For example,

he revisits the naming conventions for different types of securities issued by

UST:

| Security | Tenors | Description |

| :------ | :----------------------------- | :--------------------------------------------- |

| Bills | 4 to 52 weeks | sold at a discount and redeemed at par |

| Notes | 2, 3, 5, 7, 10 years | pay a fixed rate of interest 2X per year |

| Bonds | 20, 30 years | pay a fixed rate of interest 2X per year |

| CMB | less than 1 year | cash management bills for short-term financing |

| TIPS | 5, 10, 30 years | pay a fixed rate on a principal indexed to CPI |

| FRN | 2 years | pay a variable rate of interest 4X per year |

#### **Table 1**: Securities Auctioned and Issued by the US Treasury

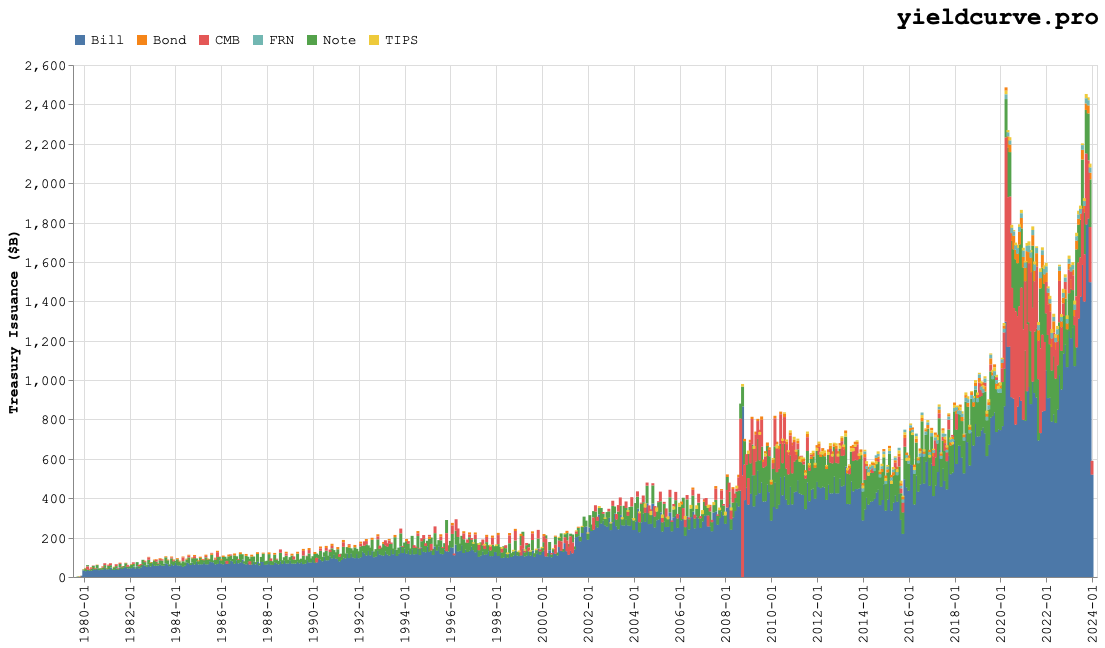

Figure 2 shows the dollar amounts of each security issued each month by UST.

#### **Figure 2**: Treasury Issuance: 1980 to the present

#### **Figure 2**: Treasury Issuance: 1980 to the present

The various maturities are rolled up for each security type and the bars are

reported, bottom up, starting with the largest dollar issuance and proceding

in decreasing order. We can see that, starting in 1980 and continuing to the

present, that Bills comprise the lion's share of UST issuance followed by

Notes.

Interestingly, there are periods where CMBs figure prominently in overall

issuance. The red regions in Figure 2 reveal that, beginning with the Pandemic

and continuing to the present, CMBs tended to outpace all security issuance

with the exception of Bills. Also, notice that they comprised almost all

issuance for a short period of time around the Great Financial Crisis (GFC).

The most notable feature of Figure 2 is the meteoric rise in issuance beginning

around early 2016 to the present. Bills, Notes, and CMBs appear to play

primary roles in UST fundraising while Bonds, TIPS, and FRNs are secondary.

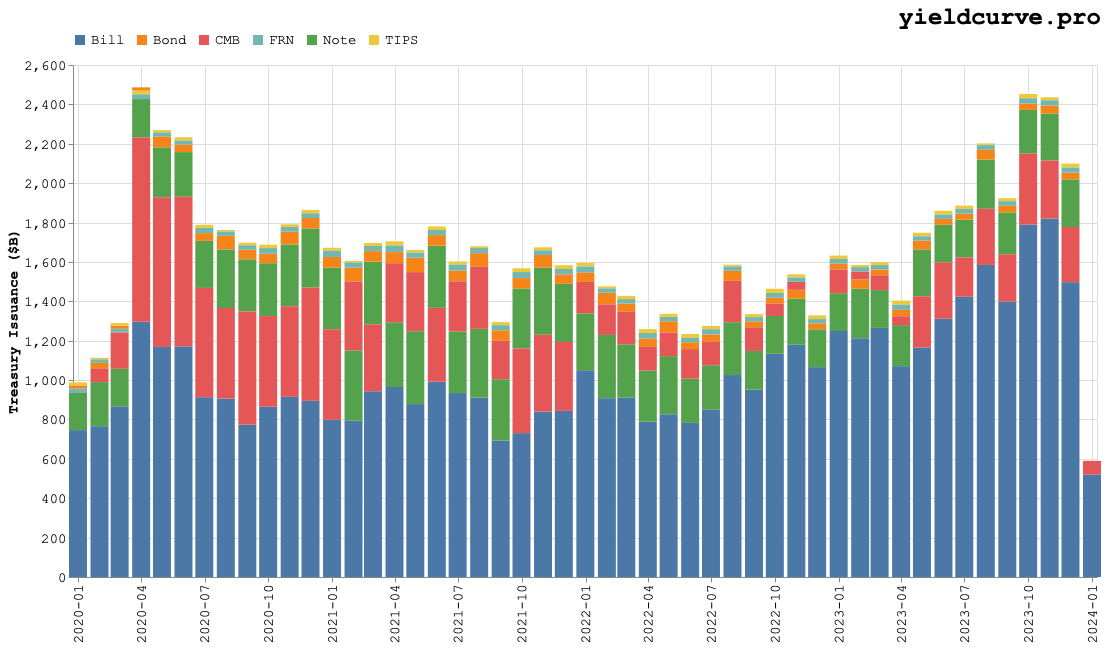

Figure 3 looks at more recent issuance data from 2020 to the present.

#### **Figure 3**: Treasury Issuance: 2020 to the present

#### **Figure 3**: Treasury Issuance: 2020 to the present

It is apparent that, depending on UST's short term cash mangement needs,

issuance of CMBs spikes and replaces Notes as the second largest security

issued. For example, at the onset of the Pandemic, issuance of CMBs increased

approximatley 5 times month-on-month from March to April of 2020.

It appears that CMB issuance only returned to relatively normal levels

almost 2 years later on January 2022. Those levels have begun to creep up

again starting May 2023. Indeed, in the first month of 2024 security issuance

has been dominated by Bills and CMBs.

It his Twitter

thread

James goes on to describe a few relatively simple statistics that auction

participants use to monitor the health of UST auctions over time.

The first one that we will consider is called the Bid-to-Cover (BTC) ratio

which compares the total dollar amount of bids over the dollar amount of bonds

sold. A BTC of 1 implies that supply (in the form of the dollar amount UST

hopes to raise) was exactly matched by demand (the bids sought by auction

participants).

Obviously, healthier auctions should have BTC greater than 1 because auctions

were over subscribed. James also explains that auction health should be

measured relative to past auction BTCs.

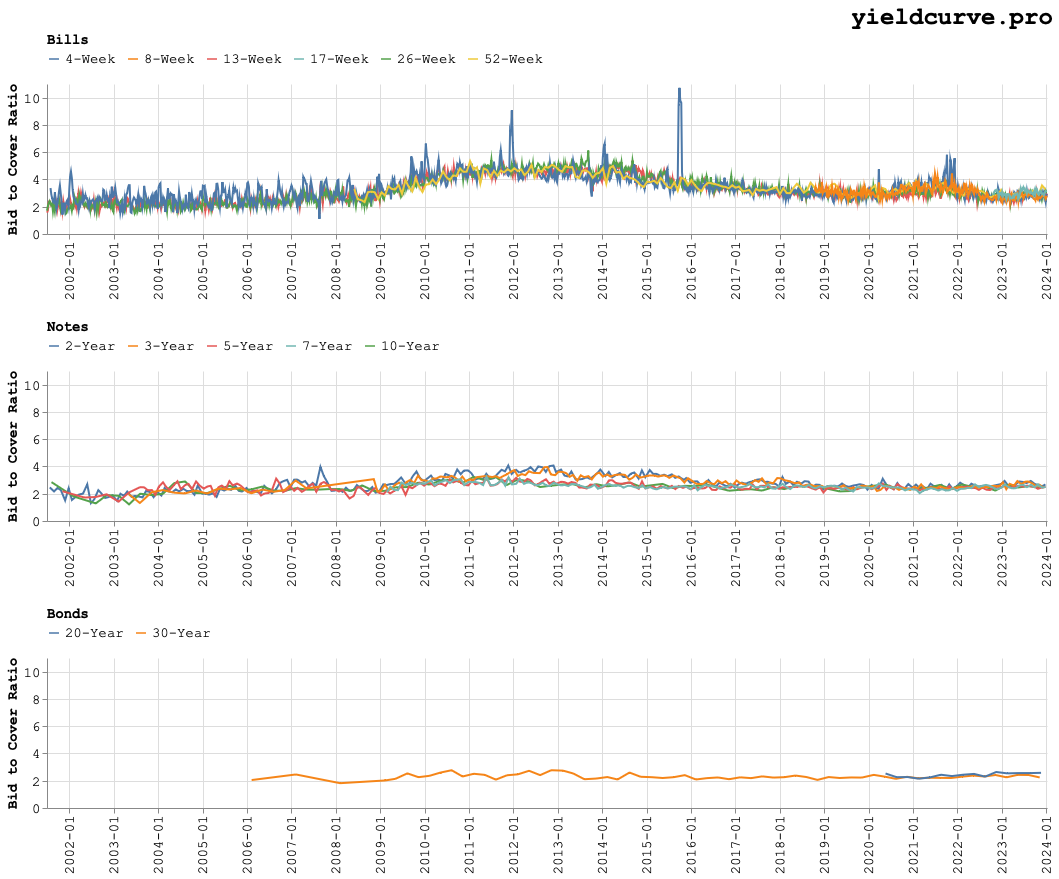

Figure 4 shows BTC for Bills, Notes, and Bonds from 2001 to the present.

#### **Figure 4**: BTC for Bills, Notes, and Bonds: 2001 to the present

#### **Figure 4**: BTC for Bills, Notes, and Bonds: 2001 to the present

Each panel in Figure 4 superimposes BTC curves at each available tenor.

Irrespective of security type or tenor, their is a remarkable level of

consistency in ratios. From 2001 until the onset of the GFC, ratios hovered

just above 2. Mid 2008 they begain to increase reaching a peak

(between 4 and 6) around 2013. From there, average BTC levels decreased

reaching roughly steady-state around 2019 with levels between 2 and 4.

What does this mean qualitatively? Perhaps that, relative to the previous

decade (2010 to 2020) auction health seems to have deteriorated while relative

to the decade before that (2000-2010) things seems relatively healthy.

To get a better sense of where ratios could be headed we drill down and

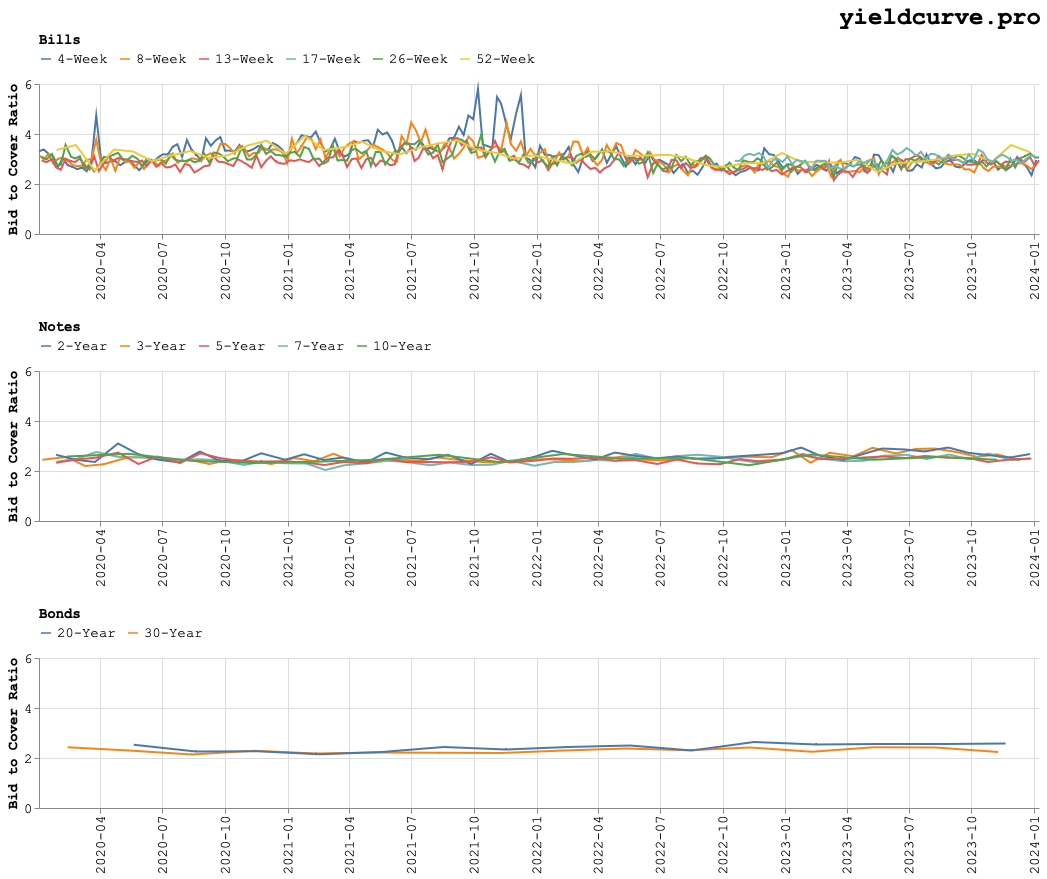

look at more recent data. Figure 5 shows BTC from 2020 to the present.

#### **Figure 5**: BTC for Bills, Notes, and Bonds: 2020 to the present

#### **Figure 5**: BTC for Bills, Notes, and Bonds: 2020 to the present

Note and Bond BTC seems to be relatively steady. However, Bill BTC does

exhibit a slight downtrend relative highs around the end of 2021. As we

have seen, Bill issuance is the workhouse with respect to UST fundraising.

Perhaps we have reason to worry. As Mr Lavish indicated in his thread, this is

a statistic well worth monitoring in the coming days.

Thank you for reading and until then!

Related reading: Bid-to-Cover Explained: What Treasury Auction Demand Looks Like Across the Curve.