# Grading US Treasury Auctions

Source: https://www.yieldcurve.pro/blog/treasury-auction-grades-001

Published: 2024-05-13

Tags: Auction, Bid-to-Coverage Ratio, Bills, Bonds, Direct Bids, Indirect Bids, Notes, Price Tail, US Treasury

_A Systematic Approach_

# A Systematic Approach To Grading US Treasury Auctions

Results from US Treasury auctions are a big deal for the fixed-income market

because they show how much people really want to buy and own government debt.

When auctions go well, it boosts confidence, potentially leading to more risk

taking in capital markets.

To figure out if the auction did well, we can compare the recent auctions to

past ones. But which data should we consider? Andy Constan, a Wall Street

veteran with decades of experience, has a YouTube video that provides

excellent background on the subject and some suggestions on which items to

consider.

We can compare Andy's approach to the following ones described by these

internet articles:

* Reading Treasury Bond Auctions

* How To Read Treasury Bond Auctions

* How To Read Bond Auction Results

## Data, Scores, and Grades

Borrowing different ideas from each approach and utilizng data provided

directly by the US Treasury, we consider the following items:

* **Tail** - This is the difference between the highest and average yield

obtained by auction participants (reported in basis points). It is indicative

of whether or not all buyers paid a similar price or did some get bonds on the

cheap. A small tail relative to history is considered better.

* **Bid-to-Cover** - This measures the total amount of bids received for a given

auction divided by the amount actually sold. Higher relative to history is

better.

* **Indirect** - This is the percentage of non-competitive bidders (typically

foreigners) placing bids through a primary dealer. They participate this way

because they are often unable or unwilling to do so directly. Higher relative

to history is better.

* **Direct** - The is the percentage of institutions who are placing bids on the

auction directly with the US Treasury. Higher relative to history is better.

We will take each individual data item and create a score based on its time

series. The first step is to construct a z-score for each factor using an

expanding window.

$$z_{it} = \frac{f_{it} - \mu_{it}}{\sigma_{it}}$$

where

$$f_{it} := i\text{-th factor at time t}$$

$$\mu_{it} := \text{expanding window ave from time 0 to t}$$

$$\sigma_{it} := \text{expanding window std from time 0 to t}$$

Next, we use the cumulative distribution function to transform the z-score to a

score between 0 and 1.

$$s_{it} = CDF\left(z_{it}\right) \; \epsilon \; \left[0,1\right]$$

Then we equally weight the factors to arrive at an overall composite

score.

$$S_{t} = \frac{1}{N}\sum\limits_{i=1}^{N}s_{it}$$

Last, we map a given factor or composite score to a letter grade via the

following table:

| Score Interval | Letter Grade |

|:-----------------|:-------------|

| (0.0, 0.1] | D- |

| (0.1, 0.2] | D |

| (0.2, 0.3] | D+ |

| (0.3, 0.4] | C- |

| (0.4, 0.5] | C |

| (0.5, 0.6] | C+ |

| (0.6, 0.7] | B- |

| (0.7, 0.8] | B |

| (0.8, 0.9] | B+ |

| (0.9, 1.0] | A |

#### **Table 1**: Mapping Scores In The Unit Interval To A Letter Grade

A score of 0 would result in a letter grade of F. This corresponds to an

auction failing and is a situation the US Treasury has never experienced.

The four factors [above](#factor_definitions) can be easily computed using data

made available by the US Treasury. This website hosts a simple

app

compiling these data, constructing the individual and composite scores, and

presenting their charts via a simple interface. Instructions on how to use

the app can be found

here.

## Examples of Recent Auctions

Figures 1 through 4 show charts for each of the [above](#factor_definitions)

data items. The auction is for a recent 13-Week Bill issuance where Treasury

raised $67B with an averagea yield of 5.24%.

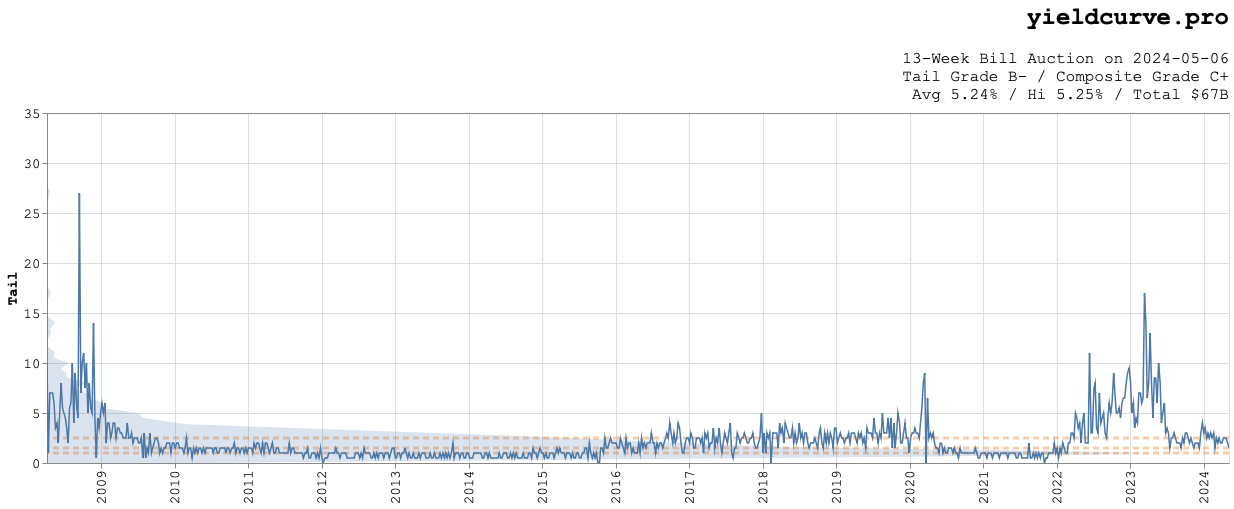

#### **Figure 1**: Tail Auction Data From April 2008 to May 2024

Based on the Tail data for the entire time period, this auction received a **B-**.

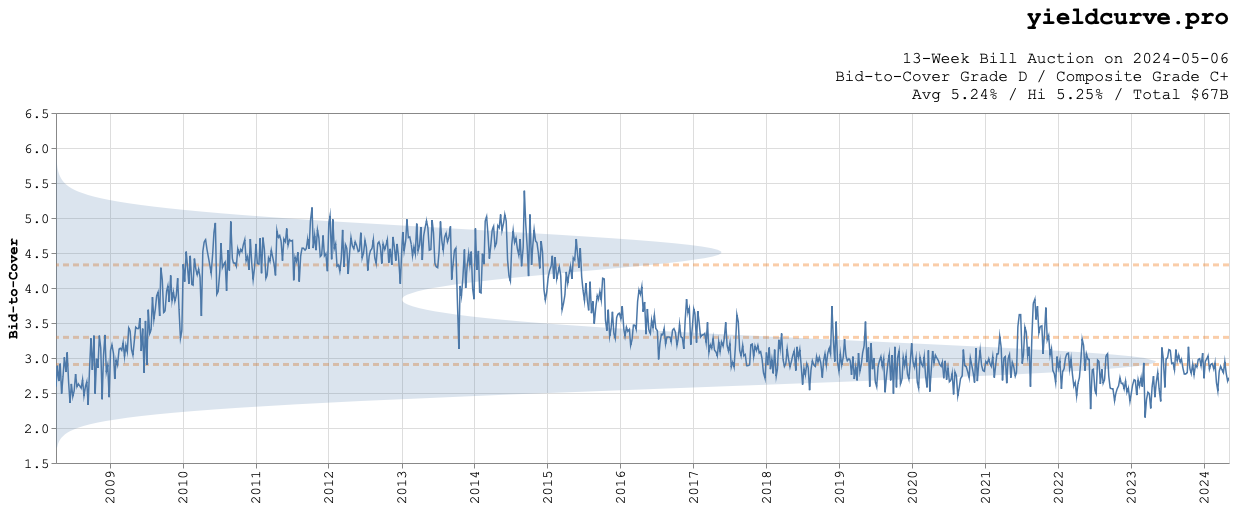

#### **Figure 2**: Bid-to-Cover Auction Data From April 2008 to May 2024

Bid-to-cover data fell well below average and earned a **D**.

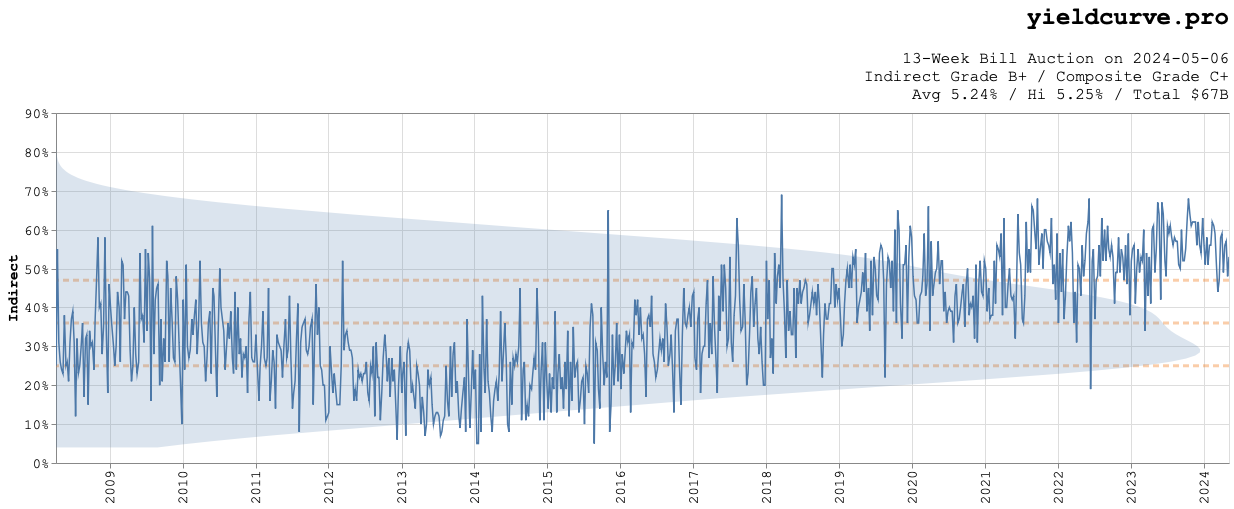

#### **Figure 3**: Indirect Auction Data From April 2008 to May 2024

Indirect ended the period above average and received a **B+**.

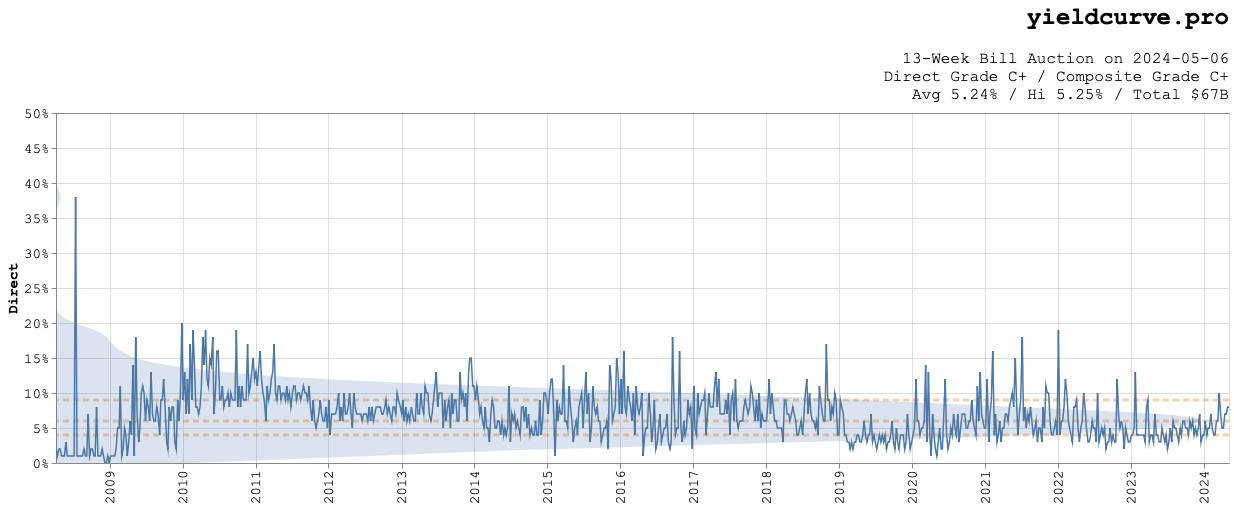

#### **Figure 4**: Direct Auction Data From April 2008 to May 2024

The Direct time-series ended the period more or less average and received a

**C+**. Equally weighting each grade, we end up with a composite grade of

**C+**, as well.

## Conclusion

The grades assigned to each auction are strongly dependent on the start and end

dates chosen for the analysis. If we care more about short term data decrease

the amount of time between the two. Feel free to experiment with the

app

and feel free to send us feedback.

Related reading: Bid-to-Cover Explained: What Treasury Auction Demand Looks Like Across the Curve.