What do current market movements in stocks and bonds have to say about 60/40 fund weights?

This is January 2024 installment of a series of post we make to track how the weights of a synthetic 60/40 stock/bond portfolio evolve intra-month. Find last month's post here.

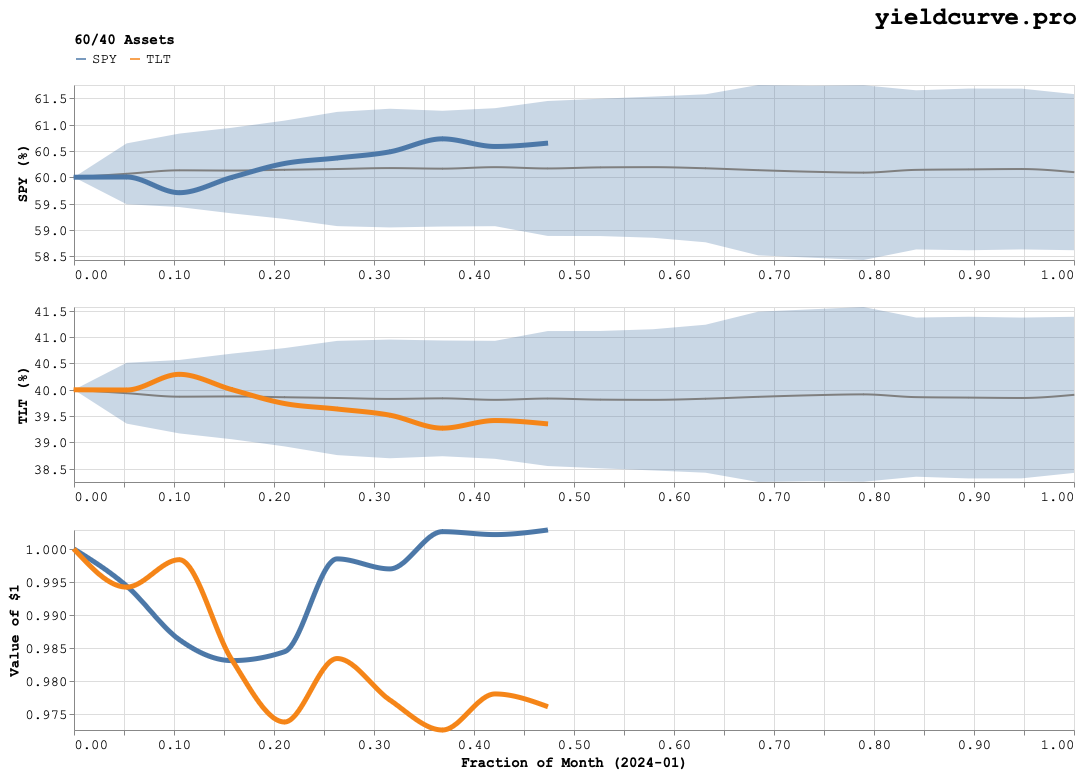

Each month we coduct a simple experiment: track the cumulative intra-month return of two stock/bond indices (say SPY and TLT). Next, combine that data to estimate a one standard deviation envelope of weights as a function of the days in the month. Then measure, for the day of the month, where the current weights sit within those envelopes. This provides a measure of how much a typical 60/40 fund needs to move in order to restore equilibrium.

Figure 1 depicts the envelopes and current weights for SPY and TLT.

Figure 1: Stock/Bond Weights For January 2024

Current deviations imply that, as of today, 60/40 funds would be sellers of stocks and buyers of bonds with moves of just over 50 basis points to restore equilibrium.

Back