Does adding gold to traditional stock-bond portfolios provide diversification (Part 3)?

In our previous posts (parts one and two) we considered whether gold diversifies a classic portfolio of equities and Treasuries. Those simple studies showed that gold can add diversification depending on the tenor of the Treasuries added to the portfolio.

Considering the question more carefully we examine the correlation (computed in excess of the risk free rate) of gold with different bond and equity ETFs show in Table 1.

| Ticker | Description | Asset Class |

|---|---|---|

| GLD | Gold | Gold |

| SHY | 1-3 Year Treasury | Bonds |

| IEI | 3-7 Year Treasury | Bonds |

| IEF | 7-10 Year Treasury | Bonds |

| TLH | 10-20 Year Treasury | Bonds |

| TLT | 20+ Year Treasury | Bonds |

| SPY | S&P 500 | Stocks |

Table 1: ETF Proxies for Gold, Bonds, and Stocks.

Figure 1 shows the rolling 1 year correlation of GLD with SPY and the fixed-income ETFs in Table 1 that cover tenors ranging from 1 to 20+ years.

Figure 1: Rolling 1 Year Correlation of GLD With Various Bond & Equity ETFs

It is interesting to note that GLD's correlations with these particular Treasury bond ETFs remain largely positive. They are also strongly cyclical. Equally interesting is to notice how GLD's correlation with SPY shows the opposite temporal characteristics while largely centering around 0. It is only in the most recent times, beginning in early 2022 around the onset of the pandemic, that the trend has been broken and GLD-SPY correlation has begun to follow its own specific path.

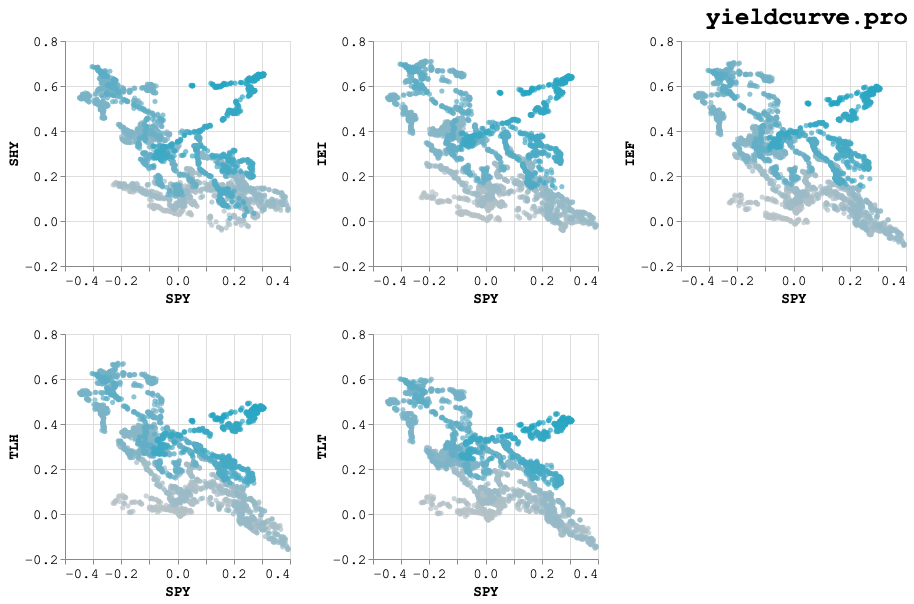

Figure 2 observes things from a different perspective by charting GLD's correlation with SPY versus its correlation with each Treasury ETF.

Figure 2: Compare GLD's Correlation With Stocks vs Bonds

The panels in Figure 2 are ordered by the increasing tenor of each ETF under consideration. Also, the color of the symbols marking each point vary from gray to blue depending on the point in time. Earlier points occur in gray while later points in blue.

Excluding the bluest points, it should be clearly evident that GLD's stock-bond correlation follows an inverse linear relationship. Specifically, as GLD's correlation with SPY increases, GLD's correlation with bonds decreases and vice-versa.

Returning our attention to the bluest points in the charts shows an interesting pattern. The upper right-hand quadrants of each chart shows a departure from the typical inverse linear pattern. These points correspond with dates beginning with the Pandemic and continuing to the present.

Another pattern that becomes apparent is that, while GLD's stock correlation tends to be restricted to a relatively consistent range (roughly -0.4 to +0.4) it's correlation with each fixed-income ETF seems to be a function of tenor. Correlations at shorter tenors tend to remain more or less positive while those for the longer tenors venture into negative territory for some dates. Therefore, the average correlation for shorter tenors tends to be higher than those for the longer ones.

This observation suggets that GLD can be diversifying (at times) for pure equity portfolios but not, generally speaking, for those containing exposure to rates. In particular, because shorter dated rates exhibit consistently positive correlation, GLD is not an efficient diversifier for these types of allocations. Portfolios with exposure to longer dated rates could benefit from an allocation to GLD but, as Figure 1 shows, it depends on where we are in the cycle.

It will be interesting to observe how GLD's correlation with SPY and the other Treasury based ETFs evolves in the near term. Will they continue to display a bit of independence or will they return to the typical pattern observed over the previous 15 years?

In any case, it seems apparent that adding gold to traditional stock-bond portfolios does not provide consistent diversification. This is particularly true for portfolios with exposure to rates with tenors less than 20 years. Therefore, it seems that gold is best used either as a speculative asset or one used to tactially diversify pure equity portfolios.

Back