How to Read Implied Forward Rates

Implied forward rates are the bond market's built-in expectations — or more precisely, the breakeven rates embedded in the current term structure. If you follow Treasury markets, understanding how to read them is essential for interpreting what the curve is actually telling you.

We recently launched an implied forward rate tool that computes and visualizes forward curves at various horizons. This post explains what forward rates are, how to read them, and how practitioners use them.

What is a forward rate?

A forward rate is the interest rate implied by today's spot curve for a future period. It is a mathematical extraction, not a forecast. If the 2-year Treasury yields 4.25% and the 3-year yields 4.35%, there is exactly one 1-year rate, starting 2 years from now, that makes those two investments economically equivalent. That rate is the 1-year forward rate, 2 years hence.

The intuition is straightforward. An investor choosing between (a) buying a 3-year bond and (b) buying a 2-year bond and rolling into a 1-year bond should be indifferent between the two if the curve is priced consistently. The forward rate is the roll rate that makes them indifferent.

More generally, for any rate tenor and any forward horizon, we can extract an implied forward rate from the current term structure. Our forward rate tool does exactly this — it computes the full forward curve at a given horizon and plots it against today's spot curve.

Reading the forward rate curve

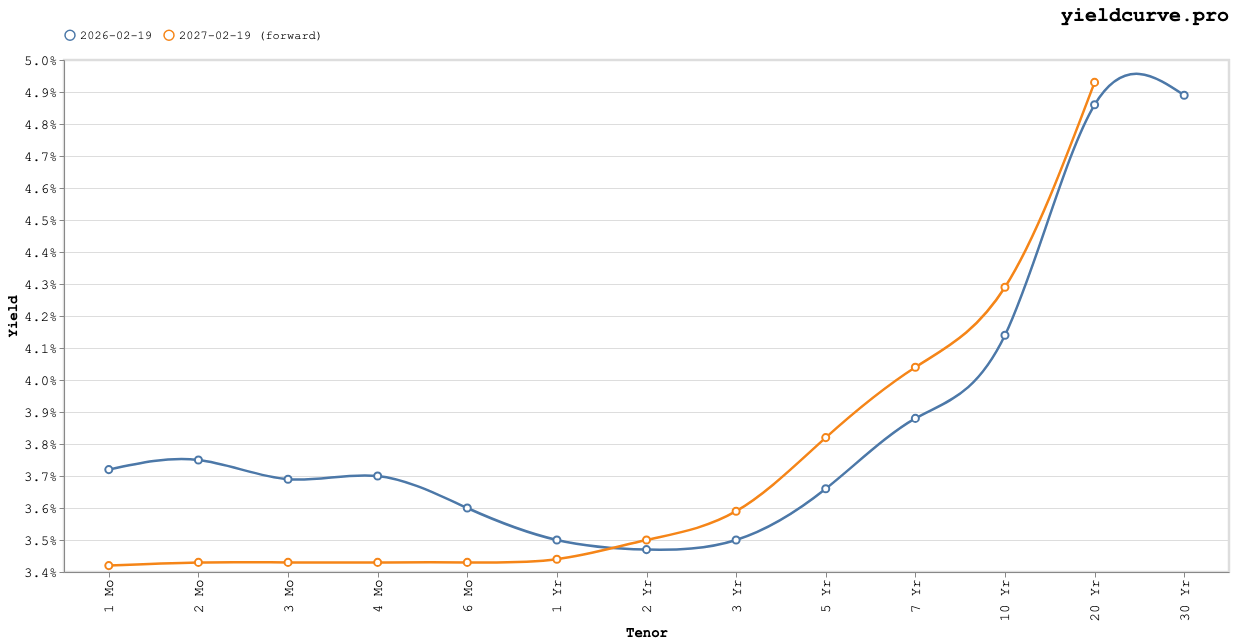

Figure 1 shows a typical output from the tool: today's spot curve (blue) versus the 1-year implied forward curve (orange).

Figure 1: Spot Curve vs. 1-Year Implied Forward Curve

There are three things to look for when comparing the forward rate curve to the spot curve:

1. Where forward is below spot: the market is pricing rate cuts.

At the front end (1 Mo through ~2 Yr), the forward curve sits below the spot curve. This means the market implies that short-term rates will be lower a year from now than they are today. In the current environment, this reflects expectations for Fed easing. The gap between the two lines at the front end is a rough measure of how much easing is priced in over the horizon.

2. Where forward is above spot: term premium is showing up.

At the long end (10 Yr and beyond), the forward curve sits above spot. The market is demanding additional compensation for holding longer duration. The steepness of the implied forward curve beyond 10 years reflects term premium — the extra yield investors require for bearing duration risk over extended horizons.

3. Where the two curves cross: the inflection point.

The crossover — typically somewhere around 2 to 3 years in the current environment — is where the net effect flips. Expected rate declines dominate at shorter tenors, while term premium dominates at longer tenors. Both components exist at every point on the curve, but the crossover is where they balance. This point moves over time and is worth watching. When it migrates left (toward shorter tenors), the market is pricing faster or deeper cuts. When it migrates right, easing expectations are being pushed out. You can track these shifts over time using the slopes and levels tools.

A classic framework

The relationship between spot rates and forward rates was elegantly formalized by Salomon Brothers in their landmark 1995 series Understanding the Yield Curve. In the second installment, they decomposed the forward rate for a given tenor and horizon into two components:

$$f = E[r] + \pi$$

where $f$ is the forward rate, $E[r]$ is the market's expected future spot rate, and $\pi$ is the term premium. This decomposition is critical because it tells us that forward rates are biased estimators of future spot rates. They consistently overestimate where rates will actually land because they embed a risk premium that compensates investors for uncertainty.

Salomon showed empirically that this risk premium is positive on average and increases with maturity — which is exactly why the forward curve tends to sit above the spot curve at longer tenors even when no one expects rates to actually rise.

What forward rates are NOT

A common mistake is treating implied forward rates as forecasts. They are not. The 1-year forward 10-year rate is not "the market's best guess" of where the 10-year will be in a year. It is the breakeven rate extracted from today's term structure — the rate that makes locking in today versus rolling over economically equivalent.

The distinction matters because:

-

Forward rates have historically overestimated future rate increases. An investor who systematically bet that rates would rise less than forwards implied — the classic carry trade — has been profitable more often than not over long horizons. That said, this relationship can invert during aggressive tightening cycles. In 2022-2023, forwards actually underestimated the pace of Fed hikes.

-

The term premium embedded in forwards varies over time. It is not constant. During QE, the Fed directly compressed term premium by removing duration supply from the market. During inflation scares or periods of fiscal concern, term premium expands as investors demand more compensation for uncertainty.

-

Changes in forward rates are more informative than their levels. If the 1-year forward 10-year rate drops 30 basis points in a week, the market is meaningfully repricing either its growth outlook, its inflation expectations, or the term premium it demands. That move tells you something. The absolute level is harder to interpret because it bundles expectations and risk premium together.

Practical uses

Forward rates show up everywhere in fixed income:

| Use Case | What Forward Rates Tell You |

|---|---|

| Fed expectations | How many cuts (or hikes) are priced into the front end |

| Carry and rolldown | The breakeven rate — if realized rates match forwards, carry earns zero excess return |

| Relative value | Whether a specific tenor is cheap or rich vs. neighbors |

| Hedging | The breakeven rate for locking in funding costs |

| Scenario analysis | What curve shape is implied at various future dates |

Table 1: Common Applications of Implied Forward Rates

For portfolio managers, the forward curve is effectively the market's breakeven. If you think rates will fall more than forwards imply, you want to be long duration. If you think forwards are roughly right, earning the carry is your edge. If you think rates will rise more than implied — a rare but important scenario — you want to be short or hedged.

Try it yourself

Our implied forward rate tool lets you select any horizon and see the full forward rate curve versus today's spot curve. Try toggling between 1-year and 5-year horizons — the difference in shape tells you a lot about how term premium scales with time.

FAQ

Is an implied forward rate the market's forecast of future interest rates?

No. A forward rate is a breakeven rate extracted from today's term structure, not a prediction. Salomon Brothers' 1995 decomposition writes the forward rate as the expected future spot rate plus a term premium, so forwards consistently overestimate where rates actually land because they embed compensation for duration risk.

How do you compute a 1 year forward rate 2 years from now from spot Treasury yields?

Equate the three year compounded return with investing in the 2 year then rolling into the implied 1 year. If the 2 year yields 4.25% and the 3 year yields 4.35%, solve $(1.0435)^3 = (1.0425)^2 (1+f)$ for $f \approx 4.55\%$. That f is the 1 year forward rate, 2 years hence.

Why does the forward curve sit above the spot curve at long maturities?

Term premium. Investors demand extra yield to bear duration risk over extended horizons, and Salomon Brothers' empirical work showed that premium is positive on average and grows with maturity. The gap between forward and spot beyond the 10 year point is a rough measure of how much term premium the market is currently pricing.

What is the fixed income carry trade and how does it relate to forward rates?

The carry trade earns the gap between forward rates and realized rates when forwards overestimate the future path of rates. Historically it has been profitable more often than not over long horizons, but the relationship inverts during aggressive tightening: in 2022 to 2023, forwards underestimated the pace of Fed hikes and the trade lost money.

Back

Sign in to leave a comment.

Comments (0)